Four weeks ago, I predicted this morning’s Bureau of Labor Statistics Employment Situation Summary would again be especially strong. Was it?

We added 431,000 net new nonfarm payroll positions, on top

of the only estimates I saw (450,000 and 455,000), not in February’s 678,000

class but still about ten times what we need for our current, reduced

population increase. Almost all of the

numbers I have been covering improved as well.

Seasonally adjusted and unadjusted unemployment fell 0.2% and 0.3%

respectively, to reach 3.6% and 3.8%. We

reached 6.0 million officially jobless people, off 300,000, of whom 787,000, of

101,000 fewer, were on temporary layoff and 1.4 million, also down 300,000,

have been out of work for 27 weeks or longer.

The two measures of how common it is for people to be working or unemployed,

the labor force participation rate and the employment-population ratio,

improved 0.1% and 0.2% and are now at 62.4% and 60.1%. The laggers were the count of people working

part-time for economic reasons, up 100,000 to 4.2 million after last time’s

400,000 gain, and average hourly nonfarm payroll earnings, up 15 cents per hour

to $31.73, less than inflation despite February’s loss.

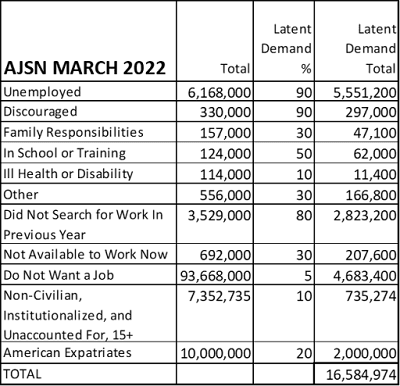

The American Job Shortage Number or AJSN, the measure of how

many new positions could be quickly filled if all knew they were easy to get,

decreased 402,000, as follows:

Compared with a year before, the AJSN has dropped almost 3.9

million, 3.4 million of that from those jobless, half a million from a lower

count of people interested in work but not searching for it for at least 12

months, and the other statuses collectively little changed.

On the pandemic front, the differences in seven-day rolling daily

averages between February 15th or 16th and March 16th all

showed the dramatic fading of the Omicron variant, with new cases down 75% to

31,216, deaths off 46% to 1,263, people hospitalized dropping 70% to 25,558,

and vaccinations, including boosters, 54% lower at 237,025. There is scant reason, and even less day by

day, to think a significant number of people are taking undue risks by

working.

So how good was it… really?

It wasn’t as super-strong as February’s, and the two-month trends of

more people counted as employed without the full-time work they want and pay raises

not covering increasing prices are causes for concern. Yet our unemployment rates are only a few

tenths of percent higher than they were just before Covid, and much of the

effect of higher oil and food prices from the Ukraine war, three weeks old at

survey time, is already baked in. How we

do from here will depend on how many of those 600,000-plus new entrants find

work. If they do, April should match or

exceed March, but if they don’t, we may more or less break even next time. For now, though, once again the turtle took a

good step forward.

No comments:

Post a Comment